- Follow us

The Longine IR Department interviewed Suzuki Yoshinobu, Vice President and CFO at OMRON Corporation (securities cord: 6645; hereafter "OMRON") about the roles of CFO, M&A strategies and business portfolio management.

Three key points presented by the Longine IR Department to investors

- OMRON's CFO functioning as more than the chief financial officer and having the perspective of CEO (Chief Executive Officer).

- The recent two M&A cases completing product lineups required for factory automation in the control equipment business.

- Business portfolio management by evaluating business based on facts (data) and future potentiality.

Longine IR Department (hereafter Longine):

I have learned about OMRON's Threefold Management comprising CEO, CFO and CTO in a talk with President Yoshihito Yamada. In this interview, I would like to know about the positioning and roles of CFO.

Yoshinobu Suzuki, Vice President and CFO, OMRON Corporation (hereafter Suzuki):

My biggest role is to evaluate financial growth strategies related to individual businesses as well as the entire group. For example, when CTO (Chief Technology Officer) brings proposals to enter new business areas, I assess its future potential while referring to the profitability of existing businesses, particularly from financial viewpoints and eventually judge whether we should do it or not. Whenever making judgment, I strive to be "the CFO having the eyes of CEO (Chief Executive Officer)" rather than simply being the chief financial officer.

Longine:

What is your special focus when you try to be "the CFO also with CEO's viewpoints"?

Suzuki:

Something I feel strong recently is that the closer you come to the top management, the more you must look at the whole picture, instead of limiting business domains. It's not about fulfilling given roles but creating them by yourself. I constantly strive to apply a bird's-eye view to the entire group to think how I should change it as a member of the top management.

Longine:

Regarding the aspect of using a bird's-eye view, how does the experience you had before assuming your CFO duties help you?

Suzuki:

I acted as the head of the automotive business for around six years from FY 2007. When I took up the post, the business had been in the red for years. Thanks to increasing demand for electronic automotive parts since around 2000, the sales was gradually increasing, but at the same time, requests from customers were becoming challenging. Trying to satisfy as many customer requirements as possible, the teams had been engaging in many difficult projects and these efforts resulted in deteriorating profitability due to unreasonable and excessive resource spending which occurred on various occasions. To solve this situation, I prioritized bringing the businesses out of deficit and devised plans accordingly. I also discontinued unprofitable business areas but kept those with future potential.

Longine:

When business reconstruction was an urgent problem, how did you manage to think about future growth strategies?

Suzuki:

When the business was in negative growth, I mentally calculated a ratio of 7 for earning profit and 3 for preparing for future growth. I spared more time for profit improvement, but I reversed the ratio (to three to seven) once the business reverted to performing in the black. The important thing is to be always conscious of growth opportunities whatever the situation might be. In the automotive field, business and product launches take as long time and you have to always look years ahead. Only seeking immediate profit doesn't work. You need a bird's-eye view in management to look at the entire auto industry and forecast the future of businesses.

Yoshinobu Suzuki, Vice President and CFO, OMRON Corporation

OMRON's M&A strategies

Longine:

To achieve Value Generation 2020 (hereafter VG 2020), OMRON group's long-term management visions, it may be indispensable to include outside resources through M&A in addition to ensuring the growth of existing businesses. What domains and approaches are involved in your investment for M&A? Could you explain by showing us your performance record so far?

Suzuki:

In VG 2020, long-term management visions of ten years, our goal is to achieve sales of over one trillion yen and a 15% operating income ratio increase by FY 2020. Achieving these goals essentially requires active exploitation of M&A and alliance projects in line with our three basic strategies. The three basic strategies aim to intensively reinforce the IA (Industrial Automation) segment centered on the control equipment business, development of emerging markets and strengthening of new businesses. Actually, we have started three-year growth activities since last fiscal year, including M&A by investing around 100 billion yen. The M&A of Delta Tau Data Systems (hereafter DT) and Adept Technology (hereafter AT), which were announced in July and September respectively, are the very examples of intensive reinforcement of our IA business.

Longine:

Please describe your emphasis on the intensive reinforcement of the IA business and aims of these M&A cases.

Suzuki:

My emphasis is on the further reinforcement of our wide-ranging product lineups and extension of sales channels. With two recent M&A cases, we were able to strengthen our product lineups. The control equipment business already had a wide range of sensor and controller products, but drive system product lines such as servomotors had been relatively small, and the robot domain was not even in our business. By acquiring DT with strength in drive system products and AT, a strong player in robot assembly, to our group, not only were we able to strengthen domains we lacked but also complete a series of product lines in all domains required for factory automation.

Longine:

What do you specifically mean by "domains required for factory automation"?

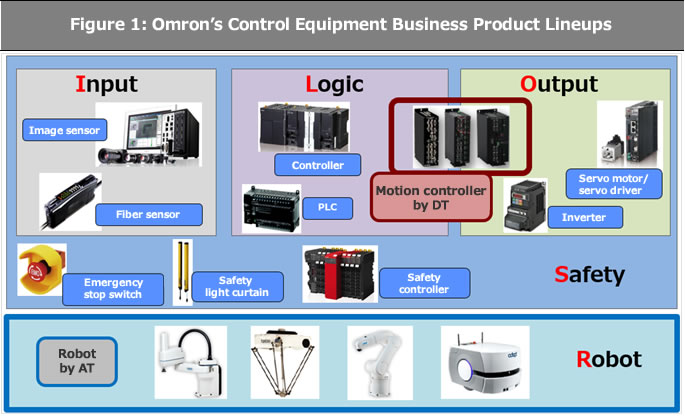

Suzuki:

Please see Figure 1. At gemba or the manufacturing shop floor, there are the Input domain where necessary information is input via sensors, the Logic domain controlled by controllers based on the input information, and the Output domain where drive systems such as servomotors carry out output. Usually two more domains of Safety and Robot are added to comprise the five domains, which need to be automated for factory automation. As you see, now OMRON can provide powerful products in each of these domains.

Source: Prepared by the Longine IR Department, based on SPEEDA and data provided by the company

Longine:

I have learned how OMRON manages business portfolio by mapping almost 100 business units on four quadrants divided by two axes of sales growth rate and ROIC (return on investment). Business portfolio management sometimes may require withdrawing from existing businesses. How is your business portfolio management used?

Suzuki:

We often become emotionally attached to a business, and withdrawal is usually a tough decision. The decision becomes even harder when remembering customers' smiles or seeing employees' faces. However, I have to make rational managerial decisions as the CFO. People at gemba want to see a rosy scenario, but I cannot let an unpromising business survive. Failure in some business segments may adversely affect the entire group performance. My portfolio management also considers such a situation. My role is to think of possibilities two or three years down the line by referring to assessments based on a fact (data) available within the group. It is also one of my responsibilities to propose whether we should or should not continue to CEO and the relevant business departments. If an appropriate decision cannot be made due to adverse reaction at the workplace, I may issue a command to withdraw.

Longine:

Is the period of three years sufficient to evaluate business? Is there any difficulty completing an evaluation within a specified period of time?

Suzuki:

We have decided that the maximum time length for a PDCA (plan-do-check-act) cycle is three years. However, using fixed time lengths may make evaluation difficult, when business environment changes rapidly. For example, there are businesses that would eventually grow after three to four years' R&D even if its possibility isn't realized immediately. In such a case, it is necessary to judge the continuation of business by considering its future potential and total optimization as a group.

Future financial strategies: Maximizing effects of growth investment and portfolio management

Longine:

Financing may be affected due to increased M&A activities in the future. How do you optimally balance your investment and financial structure including capital policies?

Suzuki:

From the viewpoint of supervising financial affairs, the concept "Cash is King" (cash is strongest) always underlies my management. Cash can be the source of relief when facing some critical situation. On the other hand, in VG 2020, a great emphasis is placed on positive creation of future business opportunities through investment for growth. We also must pursue profit growth in accordance with the scale of investment. Seen from this viewpoint, I don't think that the present financial status is something that is final and that has to be maintained.

Longine:

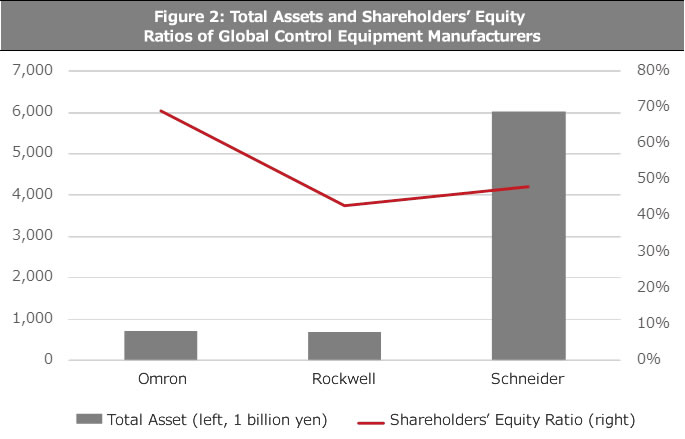

Figure 2 shows the total assets and shareholders' equity ratios of global control equipment manufacturers. OMRON's shareholders' equity ratios exceed 70% in the chart, and we can say that it has a predominantly healthy financial standing among global control equipment makers. On the other hand, your competitors expand total assets via financial leverage to develop business, regardless of their business scales. How do you address this difference?

Source: Prepared by the Longine IR Department, based on SPEEDA and data provided by the company

Suzuki:

OMRON has deployed a highly profitable business and inherited excellent assets. It will be necessary, however, to take positive risks in terms of finance in the future to extend business areas and domains by utilizing assets. We are willing to use financing leverage if it's really necessary for further growth. I'm determined to secure necessary resources and practice managerial decisions in conformity with business portfolio management, as "the CFO with the perspective of CEO".

Longine:

Thank you very much for your time today.

Suzuki:

Thank you very much.

© Copyright OMRON Corporation 2007 - All Rights Reserved.