- Follow us

The Longine IR Department interviewed Satoshi Ando, Managing Director and Executive Officer, and Global IR Corporate Communication General Manager at OMRON Corporation (securities cord: 6645; hereafter "OMRON") about the background behind favorable business achievements and future business efforts of the company.

Three key points presented by the Longine IR Department to investors

- Increase in the company forecast for both sales and profit in FY 2014 marking the highest to date.

- Sustainable "power to earn" being developed through post-Lehman shock restructuring.

- Constant growth toward the goals of over 1 trillion yen and operating income ratio of 15% in FY 2020.

Longine IR Department (hereafter Longine):

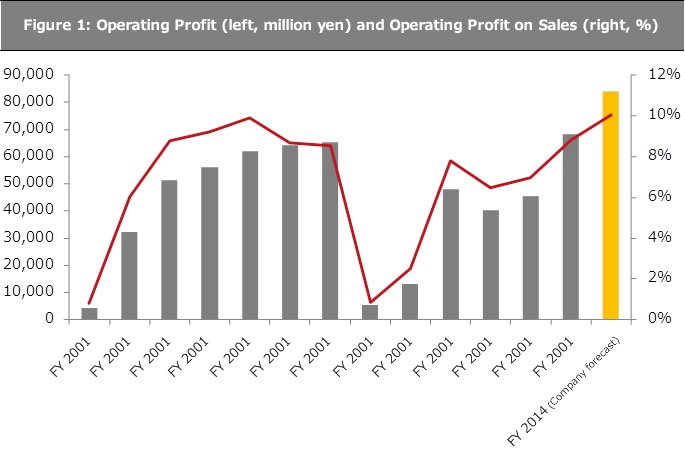

Your company announcement says that the increase in its FY 2014 sales and profit forecast has set a record to date and we at Longine are paying attention to your recent profit changes (Figure 1). Some view that the recent business results of OMRON have shown as sudden recovery particularly due to the increased capital spending as a result of a weak yen and global business cycle. Is this the case, or are there other factors related to changes in your management after the Lehman shock?

Satoshi Ando, Managing Director of OMRON Corporation (hereafter Ando):

To sum up, our management policies drastically changed after Lehman shock. Even though the sales and profit increases for six consecutive quarters until FY 2007 can be definitely attributed to external factors, I believe that our post-Lehman achievement, especially the swift recovery from FY 2011, is the result of voluntary restructuring efforts.

Longine:

Please detail your concrete restructuring efforts and results.

Ando:

First, I will show you how we began to focus on profit as a guidepost to restructuring our company as a manufacturer after the Lehman shock. We had an urgent sense of crisis that the operating income of the entire group might turn negative after the Lehman shock in 2008, when we were devising our plan. It was an extremely big shock for the company and business department management, since even the FY 2001 performance immediately after the IT bubble collapse was better: The profit for the quarter was negative but the operating income, positive.

Source: Prepared by the Longine IR Department, based on SPEEDA and data provided by the company

Longine:

What was the reaction of the management, faced with a possible crisis of operating income deficit?

Ando:

Hisao Sakuta (presently Representative Chairman and CEO of Renesas Electronics Corporation), the then president of OMRON challenged the conventional concept of manufacturing and restructured investment decision making into a top-down process for contingencies. In particular, the first action aimed to exploit OMRON's strength as a manufacturer with a self-sufficient capability to create a variety of unique products and globally distribute them.

Longine:

What changes did these measures bring?

Ando:

We focused on manufacturing products according to specifications provided by customers. That was simple, order-to-build operation by repeating the same process from "development" to "design" and "manufacturing" for every product, even for products with similar functions. We thought only following customer demands and instructions would never improve our values as a manufacturer and that is why we had to radically change our way of thinking on manufacturing after the Lehman shock.

Satoshi Ando, Managing Director and Executive Officer at OMRON Corporation

Longine:

Could you detail your efforts in that context?

Ando:

Let me show you a company jargon: a concept called "CMO" and coined by the aforementioned Sakuta and promoted throughout the company with an indomitable resolve to change. The term is the acronym of "Common, Module and Option". "Common" refers to common platforms created to accommodate multiple products with the same function. However, only common functions alone cannot completely meet specific customer demands and therefore, optional features are required in the form of "Module". Modules are provided as "Option". In other words, this approach based on maximum common parts utilization can reduce manufacturing costs while enhancing production efficiency and surmount the post-Lehman shock situation. We can increase our profit by focusing on the profit rate even when we cannot expect an increase in sales.

Longine:

Were there other measures OMRON persistently pursued to maintain profitability, taken alongside a change in the way how manufacturing is defined?

Ando:

A special emphasis was also placed on gross margin rates (rough profit rates) as a management index. This effort was powerfully promoted by Yoshihito Yamada, the current CEO and then Managing Director and Executive Officer, Group Strategy Section General Manager and the right hand of President Hisao Sakuta.

Longine:

Special focus on gross margin rates seems quite natural for a manufacturing company like OMRON…

Ando:

Maybe so. However, the fact was that we used to prioritize cost price rates over gross margin rates as an evaluation index.

Longine:

Gross margin rates and cost price rates are just like the two sides of a coin. Why do you have to consider them as two completely different things?

Ando:

For example, the sales department persistently requests "cost reduction" to the manufacturing department to enhance price competitiveness of new products to be launched. Upon receiving this request, the development and manufacturing departments make every possible effort and resource to review the designs and material procurement, which may lead to cost reduction. However, the lack of understanding the importance of enhancing added values may lead to disregarding the necessity of fair pricing and may eventually to the failure to improve product-specific profits. All responsibilities may fall upon efforts by the development and manufacturing departments, if cost price rates are used as the index. Therefore, a shift was made to use gross margin rates as the index, based on profit rates for every product, which was also connected to the sales department. Even though they may appear to be "the front and back sides of a coin", the meaning of these figures is very different.

Longine:

A shift from cost price rates to gross margin rates aims to involve all departments including the sales function, right?

Ando:

Exactly. If we only focus on cost price rates, we may lose sight of values pursued throughout the process from planning, to development, manufacturing and sales. After the shift, however, each department began to see things from the same standpoint and became more conscious about maximizing profit by prioritizing gross margin rates.

OMRON's results seen from the managerial point of view

Longine:

How do you evaluate your results in the context of manufacturing business with "power to earn"?

Ando:

The gross margin rate already hit the bottom in FY 2008 and is recovering. It was 34.8% in FY 2008, and is expected to improve to 39.6% according to the FY 2014 forecast. But there is another management index we use besides gross margin rates. We also emphasize our ROIC (return on investment) rates.

Longine:

Some readers may not be familiar with ROIC, compared with ROE we often hear of. What kind of index is it?

Ando:

Profits in fixed periods of time such as gross margin rates are important in business. On the other hand, it is necessary to evaluate profits in terms of the return on capital investment. Since we are a manufacturing business, we want to focus on in-house manufacturing of high-quality products. Therefore, an index to evaluate our performance both in terms of profit (flow) and investment (stock) is ROIC.

Longine:

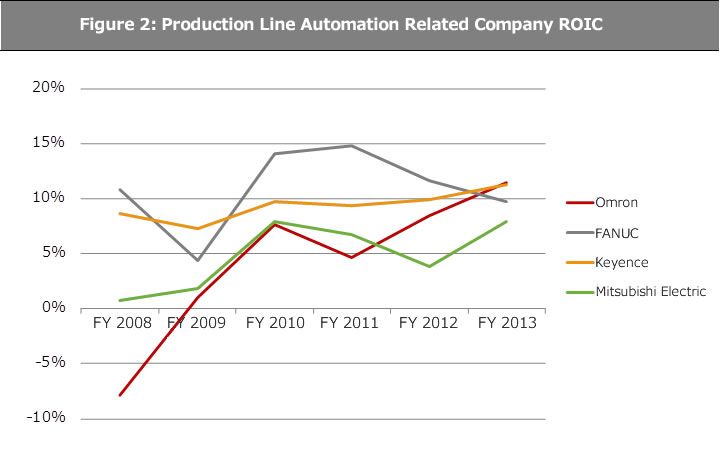

Figure 2 shows ROIC rates of Japanese companies related to production line automation called FA (Factory Automation). Despite some fluctuations, OMRON's ROIC definitely shows a gradual recovery from the bottom in FY 2008. The curve even suggests that OMRON stands out among other control equipment-related companies. How do you predict its future improvement?

Ando:

The gross margin rate is an important value driver to improve ROIC. We also set key performance indicators (KPI) specifically for every business and function organization to improve the gross margin rate. By engaging individual organizations to set appropriate indices for themselves, we can evaluate their performances regularly, use them to identify and solve problems as well as plan our future business strategies.

Source: Prepared by the Longine IR Department, based on SPEEDA

Note 1: ROIC = The average of Quarterly Net Incomes ÷ (Net Assets + Interest-Bearing Debt).

Note 2: The FY 2012 value for Keyence uses a rolling 12 months value.

Longine:

It's a well-known fact that top management in general has difficulty encouraging employees to share the importance of appropriate indices to achieve the profit and degree of improvement the company aims at. At OMRON, all employees share their immediate indices to improve its ROIC by engaging themselves in achieving goals, don't they?

Ando:

You're right. Even if the management recognizes the importance of ROIC and ROE, they usually find it difficult to let it be known throughout the organization. Our practice to improve management called "ROIC management" may provide a good reference for other companies. In fact, we have received the Grand Prix (the highest award) in "the FY 2014 Corporate Value Improvement Commendation" hosted by the Tokyo Stock Exchange. It is a great honor for us to be awarded the best evaluation among over 3,400 listed companies, and I believe this can be attributed to our "ROIC management".

Longine:

What advantages do you think ROIC has?

Ando:

Our company operates a wide range of businesses from control equipment to health care business. Most customers in the control equipment business are companies while those in the health care business are individuals. Many stockholders and analysts used to say that evaluating values represented by the entire group is difficult due to its business diversity. However, using ROIC has enabled the objective assessment and evaluation of capital productivity. Corporate values are not about the business scale (sales) or profit size. ROIC is an index that can provide fair evaluation and reasonable criteria used to allocate precious managerial resources throughout the company. It can also promote awareness among the management and individual employees that they can enhance business values and shareholder values by constantly achieving positive returns on shareholders' equity cost through daily business operations as a listed company.

Longine:

You have increased profit steadily and smoothly after the Lehman shock. How do you think OMRON can continue its growth from now onward?

Ando:

In our mid-term plan, we have specified target values including sales of more than 900 billion yen, sales gross profit rate of more than 40%, and operating income ratio of more than 10% and ROIC of more than 13% for FY 2016. As long-term goals, we envision sales of more than 1 trillion yen and a 15% operating income ratio in FY 2020.

Longine:

What are your concrete actions to achieve target values?

Ando:

They are three-fold. The first aspect is active investment to develop the control equipment and electronic component business and increase global sales. The second is active deployment in emerging markets such as China, ASEAN, India and Brazil. In this sense, growth in the health care business will be very notable. The third is reinforcement of new businesses. In particular, we are concentrating on accelerating growth in environmental-related businesses. The power conditioner segment for example, indispensable to photovoltaic power generation, has marked a rapid progress and flourished to gain the top national share in these three years.

Longine:

What are your thoughts on non-continuous growth, namely, growth by mergers and acquisitions (M&A)? Some control equipment companies, particularly overseas, are expanding their business scale through active M&A. Huge M&A is also carried out in the automotive industry. The health care industry is not an exception, where many M&A cases take place. How will OMRON cope with such a business environment?

Ando:

We concentrate on M&A and business alliance (tie-up), in addition to reinforcing existing operations in control equipment, electronic component and health care business. We have already purchased some businesses, and will accelerate such strategic investment including M&A in the future by allocating the funding of around 100 billion yen in three years.

Longine:

The market capitalization of OMRON has already exceeded 1 trillion yen. Its sales aim for over 900 billion yen in FY 2016. Is 100 billion yen or so enough for M&A and alliance funding?

Ando:

100 billion yen is not meant to be the upper limit. Our equity ratio has reached nearly 70% at the end of December 2014, and we have ample net cash funds (cash and cash equivalents) amounting to 83 billion yen. We intend to positively engage in financing whenever funding is required, since we are capable of procuring considerable sums while maintaining the present financing rating. If we can continue growing steadily in the future, the rating will rise and financing options will increase.

Longine:

Is there any way you can accelerate decision making on M&A?

Ando:

Before the Lehman shock, investment including M&A inevitably was performed at an "individually optimized level", due to the company system respecting business autonomy. In other words, investment was only determined within the range of surplus resources of each company. However, optimized investment judgment from a group-wide viewpoint is now possible, thanks to the shift to "matrix management", in which the head office and business functions are organically linked and President Yamada owns the full authority to allocate resources particularly for company growth. Not to mention bottom-up inputs from business functions, the company requires a top-down decision system, which enables us to carry out necessary investments based on a bird's-eye view of our positioning against global competitors.

Shareholders return measures

Longine:

Finally, could you explain OMRON's shareholders return measures?

Ando:

We formulate very clear shareholders return rules and disclose them in a highly transparent way. In FY 2014, we have secured more than a 25% increase in dividend payout ratio stockholder, while promising to raise it to 30% by FY 2016. In addition, if our cash reserves exceed a target specified in the mid-term plan, we will immediately perform shareholders return measures including stock buybacks. We have increased dividend payments according to our basic policies, while carrying out investment for growth. Last October (in 2014), we re-purchased our stocks after a while since the Lehman shock. I believe you can expect a continuous growth and even more reinforced shareholders return measures.

Longine:

Thank you for your time today.

Ando:

The pleasure is mine. Our management is based on a strong faith, "We can achieve sustained growth as a company by creating innovation through business and contributing to global social development". All our businesses focus on high-growth areas. I have talked today mainly about how in a big pinch like the Lehman shock, we considered it an opportunity, and how our management restructuring led us to this post-shock growth. We are happy and ready to show our intrinsic values and strength in more detail in talks to follow.

© Copyright OMRON Corporation 2007 - All Rights Reserved.